So much for the new Fall season and even the return of National Football League telecasts.

Ad investment in national linear TV in October shrunk significantly from one year ago. But, heading into the holiday season, October had the highest investment in linear television compared to the rest of 2022 to date.

That’s the prunes-to-cherries assessment of the advertising landscape for free-to-air television courtesy of Standard Media Index.

National Linear TV ad spend was down 8% compared to October 2021.

SMI bases its assessment of ad spend based on actual invoicing data from all major holding companies and most major independents, representing 95% of national brand ad spend.

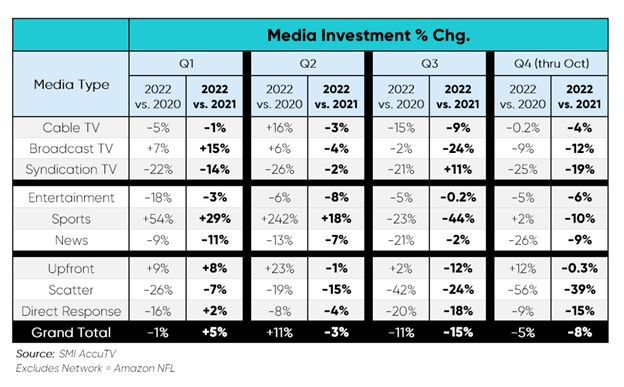

And, SMI also broke out cable, syndication and broadcast trends for October, shown below in the column on the far right.

Cable was relatively flat versus 2020 and slightly down year-over-year. Meanwhile, broadcast TV and syndication were each down from both 2020 and 2021 in a significant way.

Meanwhile, while the Upfront marketplace remains resilient, the Scatter market is extremely challenges, as is Direct Response, which had been strong through March 2022.

What happened? SMI says the Upfront/Scatter split reached an “unprecedented” 80%/10% of monthly National TV ad dollars in October.

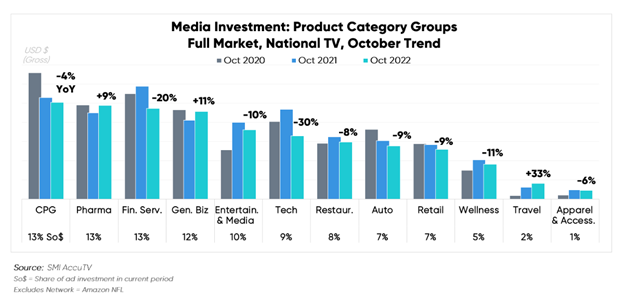

SMI also examined key advertising categories and, as was shared by MAGNA, CPG media investment is on the decline. If not for Pharmaceutical dollars, “general business” activity would be the strongest category for October.