Last year, the big story in U.S. advertising land was that, for the first time, the share of budgets dedicated to digital advertising surpassed TV spending, notes MoffettNathanson senior analyst Michael Nathanson.

While conventional wisdom might have assumed that TV’s loss was digital’s gains, the more accurate story from Nathanson is that digital is being fueled by “an army of small and medium-sized advertisers” who have benefited from the efficient targeting capabilities of Facebook and Google.

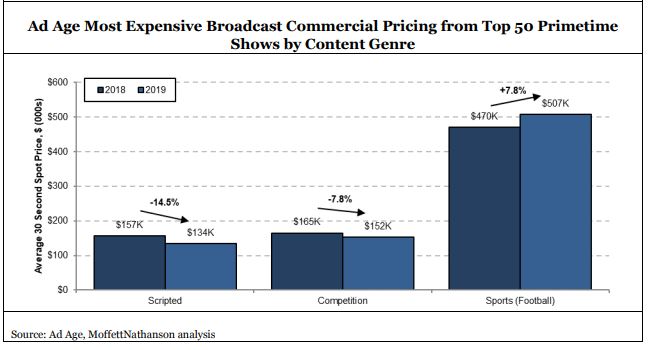

This year, Nathanson notes, “We are witnessing a further bifurcation of TV advertising along the same fault lines that we see in affiliate fee pricing power. The average unit cost of advertising in live broadcast sports content is accelerating just as the value of advertising in linear scripted broadcast shows is falling. This dichotomy will have profound impact on the long-term health of prime-time models and could force other networks (hello, ABC) to follow Fox’s winning playbook.”

As Nathanson sees it, linear national TV networks have been able to offset declines in viewing with CPM inflation “for the longest time.”

With few alternatives to find brand safe inventory in a full sound, sight and motion environment, the largest U.S. advertisers continued to maintain their budgets. As a result, CPMs continued to expand.

“Now, as cord-cutting puts even greater pressure on linear TV ad revenues, we are starting to see non-sports TV budgets shift to AVOD and advanced TV platforms,” Nathanson says. “No doubt, this will increase in the coming years.”

That’s why MoffettNathanson, post-Q3, is lowering its 2019 total U.S. ad revenue growth estimate by 130 basis points to 5.2% (vs. 6.5% previously).

There’s also a dip in digital ad growth in the forecast. But, it’s hardly headline-grabbing.

“Given the deceleration in IAB U.S. digital ad revenues over the first half of the year (driven by both weaker desktop and maturing social media), we are lowering our

2019 Internet ad revenue growth estimate by 300 bps to a still healthy 18% (vs. 21%

previously),” Nathanson says.

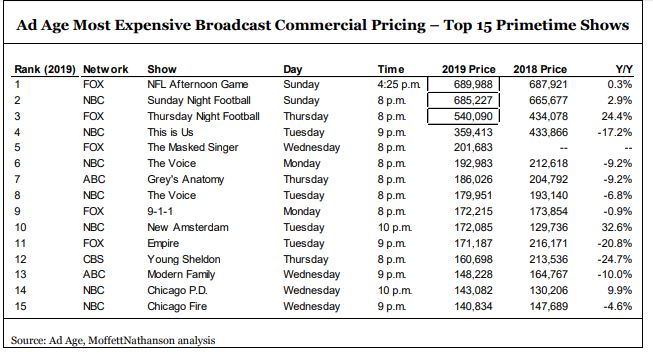

Nathanson looked at the prices and change in broadcast commercial unit rates across three content genres: sports, competition reality and scripted.

“Not surprisingly, the NFL on broadcast occupied the three most expensive commercials on the list led by FOX’s late afternoon Sunday game, NBC’s Sunday Night Football and FOX’s Thursday Night Football,” he notes.

The graphic makes CBS look exceptionally weak in terms of ad revenue against FOX and NBC, while ABC is being paced by programs with considerable longevity in its prime-time lineup.

It also puts an exclamation point on how live sports is the only genre on broadcast television, aside from local programming, that is showing growth for a network-affiliated station.

By major media type, TV declined by 4% in the quarter, driven by Cable MSOs (11%),

Broadcast Networks (6%) and TV Stations (4%), with Cable Networks remaining flat year-over-year.

What about other “traditional” media?

While Outdoor (9%) continued its streak of positive growth, Print media struggled

with declines at consumer magazines (-12%) and newspapers (-13%).

Radio “managed to squeeze out positive growth in Q3” of 2%.

Nathanson says this was “likely helped by digital.”

![]()